Several parties are involved in an international shipment.

There is usually a seller, a buyer, a carrier, a freight forwarder, a customs representative and, in some cases, an insurer or a warehouse.

But when a document is missing, when a declaration is incorrect or when goods are held by customs, one question quickly arises:

Who is responsible?

The answer depends on several factors: the commercial contract, the chosen Incoterm, the role of each party, the documents provided and the type of customs representation used.

For a company, this is a key issue.

An international shipment is not secured only by choosing the right transport solution. It is also secured by clearly defining responsibilities.

Why does this matter?

Customs is not just an administrative formality.

It is a step that can directly affect the timing, cost and compliance of an international shipment.

Before goods can enter or leave a territory, they must be declared according to the applicable rules. In the European Union, a customs declaration is an official document that provides details of the goods being imported or exported.

In France, customs authorities also specify that customs formalities can be carried out by a customs representative, either under direct or indirect representation.

The problem is that many companies do not always know who is responsible for what.

As a result, documents arrive too late, the customs code is not properly validated, the Incoterm is misunderstood or the role of the freight forwarder is overestimated.

In these situations, the shipment can slow down.

The key parties in an international shipment

To understand responsibilities, you first need to identify the roles.

In most operations, five parties are at the centre of the process.

1. The exporter

The exporter is the company that sells or ships the goods from the country of departure.

They normally know the product, its origin, composition, value and commercial documents.

In an international shipment, the exporter generally has to provide the information required for the goods to leave the country.

This may include:

- commercial invoice;

- packing list;

- product description;

- country of origin;

- required certificates;

- documents requested by the buyer or the freight forwarder.

Depending on the chosen Incoterm, the exporter may also be responsible for export customs clearance.

2. The importer

The importer is the company that brings the goods into the country of destination.

Its role is often underestimated.

However, the importer is generally responsible for ensuring that the import operation is compliant in its own country.

It must check that the goods can legally enter the country, that the documents are consistent and that duties and taxes are correctly handled.

The importer must specifically check:

- HS code;

- origin of the goods;

- customs value;

- EORI number, if the import takes place in the European Union;

- required certificates or licences;

- product restrictions;

- information provided to the customs declarant.

If this information is incorrect or incomplete, the declaration may be corrected, delayed or subject to customs control.

3. The carrier

The carrier is responsible for the physical movement of the goods.

This may be a shipping line, an airline, a road haulier, a rail operator or a multimodal transport provider.

Its role is to transport the goods according to the agreed conditions.

The carrier may also provide certain transport-related data:

- transport reference number;

- bill of lading;

- air waybill;

- CMR consignment note;

- information on the means of transport;

- departure and arrival dates.

However, the carrier is not automatically responsible for the commercial or customs content of the goods.

It does not always know the exact composition of the product, its customs classification or the specific regulatory obligations that may apply.

4. The freight forwarder

The freight forwarder organises the international shipment.

It coordinates the different parts of the chain: transport, documents, partners, formalities, tracking and, in some cases, insurance or storage.

Its role is operational.

It can help the company choose a route, compare transport modes, anticipate lead times and prepare documents.

But the freight forwarder does not replace the company in all its responsibilities.

It works with the information provided by the client, the supplier and the other parties involved.

If the initial data is incorrect or incomplete, the freight forwarder can alert the company, but it cannot invent the correct product information.

This is an essential point.

5. The customs representative

The customs representative carries out customs formalities.

In France, a customs representative can act in two ways:

- under direct representation: acting in the name and on behalf of the company;

- under indirect representation: acting in its own name, but on behalf of the company.

This distinction is important, because it can affect the level of responsibility of both the representative and the company being represented.

How do Incoterms influence customs responsibilities?

Incoterms define how costs, risks and obligations are divided between the seller and the buyer in an international shipment. They specify who organises the transport, who handles certain formalities, who bears the risks and who pays the costs related to the operation.

Choosing the right Incoterm is therefore essential to avoid misunderstandings.

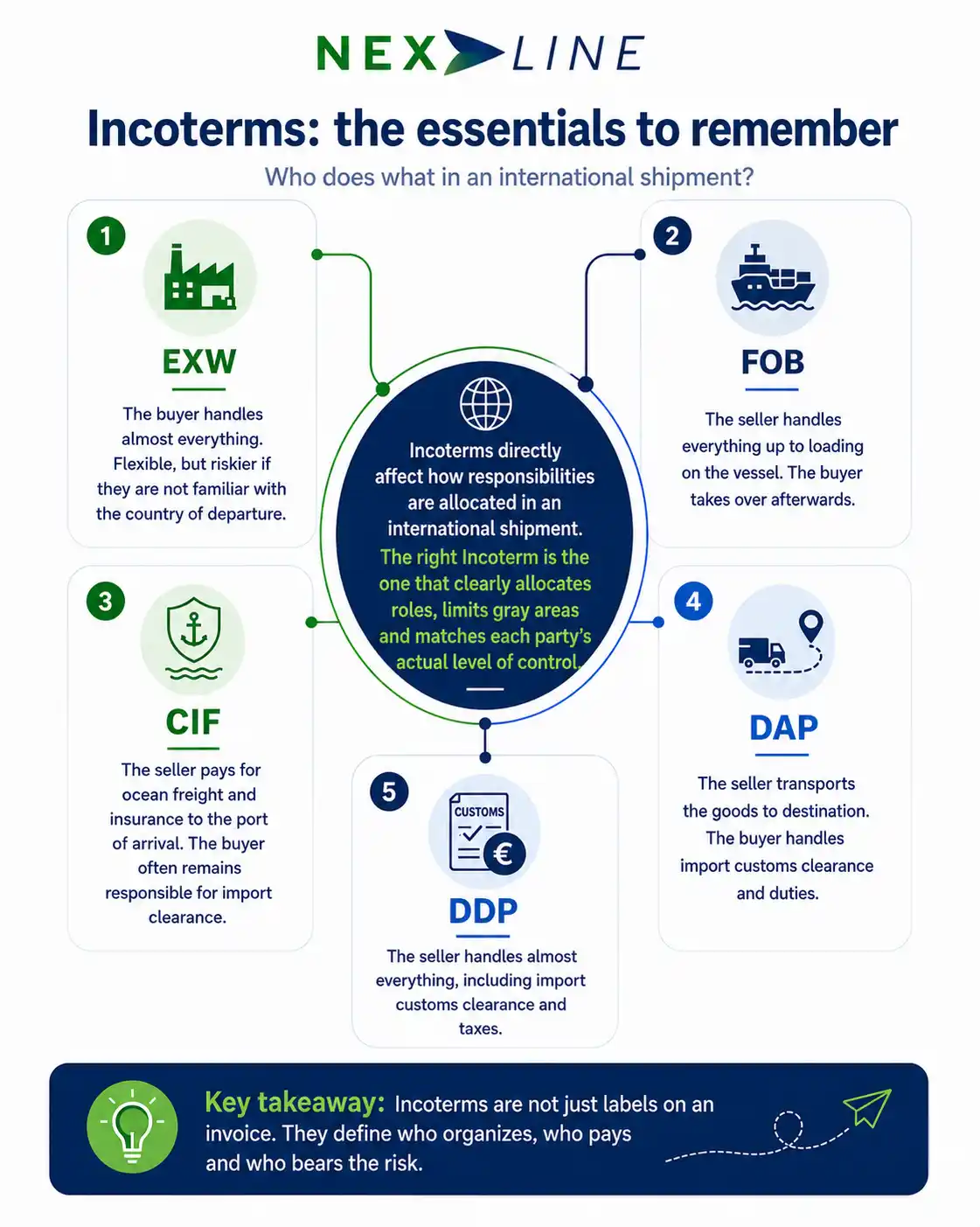

Responsibilities are not the same under EXW, FOB, CIF, DAP or DDP.

The Incoterm must be confirmed before shipment, based on the goods, the countries involved, the transport mode, the experience of the parties and the customs constraints.

What are the most common Incoterms in an international shipment?

Each Incoterm distributes responsibilities differently between the seller and the buyer.

Here are the most common cases to know.

EXW: the buyer takes on almost the entire organisation

Under EXW, the seller simply makes the goods available at its premises.

The buyer must then organise collection, inland transport in the country of departure, export formalities, international transport, import customs clearance, duties and taxes, and final delivery.

For a French buyer, EXW may look attractive because the purchase price is often lower. But it is also one of the most demanding Incoterms.

Its main advantage is control. The buyer can choose its providers, negotiate transport and manage the operation from end to end.

But the limits are significant. The buyer must handle formalities in the country of departure, coordinate collection from the supplier, manage export documents and take on more operational risk.

In practice, EXW can be risky if the buyer does not have a reliable partner locally.

Example: a French company buys goods under EXW Shenzhen. The supplier prepares the products at its factory. But the French buyer must organise everything else: collection, export documents, international freight, import into France and final delivery.

FOB: the seller manages the goods until loading on board the vessel

Under FOB, the seller is responsible for the goods until they are loaded on board the vessel at the agreed port of departure.

The seller generally manages transport to the port, export formalities and loading onto the vessel.

The buyer then takes over responsibility. It organises the main sea freight, insurance if required, import customs clearance, duties and taxes, and final inland transport.

FOB is common in maritime transport, but the transfer point must be clearly understood: the seller manages the operation up to the vessel, then the buyer takes over.

CIF: the seller pays for sea freight and insurance to the port of arrival

Under CIF, the seller organises and pays for sea freight to the agreed port of destination. The seller must also take out minimum insurance to cover the goods during maritime transport.

This is an important difference from FOB.

Under CIF, the seller pays the cost of sea freight and insurance up to the port of arrival. However, the risk is generally transferred to the buyer once the goods are loaded on board the vessel at the port of departure.

This means that the seller pays for part of the transport, but the buyer may already bear the risk during the sea journey.

At arrival, the buyer generally remains responsible for import customs clearance, duties and taxes, unloading depending on the agreed conditions, and final delivery.

Example: a French company buys goods under CIF Le Havre. The seller organises sea freight to the port of Le Havre and takes out insurance. But the buyer then has to manage import formalities, duties and taxes, and final delivery.

CIF can be useful if the buyer wants the seller to organise sea freight. However, the real level of insurance, arrival costs and exact contractual responsibilities must be checked.

DAP: the seller transports to destination, but the buyer manages import customs

Under DAP, the seller organises transport to the agreed place of destination.

This place may be a warehouse, factory, store or specific address in the country of arrival.

However, under DAP, the seller does not generally handle import customs clearance, duties or taxes at arrival.

These remain the buyer’s responsibility.

Example: a French company buys goods under DAP Lyon. The supplier organises transport to Lyon. But on arrival in France, the buyer must manage import customs clearance and pay duties and taxes.

DAP can give the impression that “everything is included”. In reality, the seller organises transport to destination, but import customs usually remains the buyer’s responsibility.

DDP: the seller takes on almost the entire shipment

Under DDP, the seller organises transport to the agreed place, handles import customs clearance and pays duties and taxes.

For the buyer, this is often the most comfortable option.

The goods arrive already customs-cleared, with fewer procedures to manage on the importer’s side.

However, DDP is very demanding for the seller. The seller must understand the rules of the importing country, be able to pay duties and taxes, manage local formalities and anticipate regulatory constraints.

DDP can therefore be practical for the buyer, but it is not always suitable for the seller if they do not know the destination country well.

How to choose the right Incoterm for your goods

The right Incoterm depends on the level of control required, the mode of transport, the country of departure, the country of arrival and the type of goods.

An Incoterm should not be chosen only because it is common or because it seems cheaper.

For fragile, sensitive or high-value goods, the choice must be even more careful.

The company should check:

- who packs the goods;

- who organises the main transport;

- who chooses the carrier;

- who bears the risk during transport;

- what level of insurance is provided;

- who manages export formalities;

- who manages import formalities;

- who pays duties and taxes;

- who responds in case of damage, delay or customs inspection.

For fragile goods, it may be better to avoid an organisation that is too fragmented between poorly coordinated parties.

The objective is to choose an Incoterm that provides good control over transport, insurance and handling conditions.

For example, if the seller knows the product and its packaging constraints very well, it may make sense for the seller to retain responsibility up to a more advanced point in the transport chain.

By contrast, if the buyer has a reliable freight forwarder and wants to control the entire logistics chain, it may prefer an Incoterm that gives it more control.

In all cases, the choice must be consistent with the value of the goods, their fragility, the risk of disruption, customs obligations and the experience level of the parties.

Who is responsible for the documents in an international shipment?

In an international shipment, the documents must be consistent with one another.

The commercial invoice, packing list, transport document, customs declaration, HS code and origin must all describe the same goods.

If information is vague, incorrect or contradictory, the risk of delay or customs blockage increases.

Responsibility depends on the source of the error.

The supplier must provide reliable information. The importer must check critical data. The freight forwarder can coordinate and alert, but it cannot invent information that has not been provided.

What the supplier must provide

The supplier knows the goods. It must therefore provide the information required for shipment and customs clearance:

- commercial invoice;

- packing list;

- precise product description;

- country of origin;

- composition or material of the product;

- certificates required depending on the goods;

- technical information if the product is regulated.

A vague description such as “parts”, “accessories”, “equipment” or “goods” can create a problem.

A good description should explain what the product is, what it is used for and what material it is made of.

What the importer must check

The importer should not simply receive the documents.

It must check the information that affects the import operation:

- HS code;

- origin;

- customs value;

- EORI number;

- duties and taxes;

- possible licences;

- product restrictions;

- applicable standards;

- documents required for customs clearance.

The importer is often the best placed party to know whether the goods can be sold, used or distributed on its market.

What the freight forwarder can do

The freight forwarder coordinates the international shipment.

It can organise transport, request corrections, check the general consistency of the documents and alert the company if information is missing.

But it works with the data provided by the company, the supplier and the partners involved.

If the product description, use or customs classification is incomplete, the risk of blockage increases.

Who is responsible for the HS code?

The HS code is used to classify the goods in the customs nomenclature. It influences customs duties, taxes, restrictions, required documents and possible inspections.

The supplier may suggest an HS code.

The freight forwarder may provide an operational view.

The customs representative may check the consistency of the declaration.

But the importer must verify that the code used actually matches the imported product and its intended use.

An HS code error can lead to a declaration correction, a customs clearance delay, an additional inspection, incorrect calculation of duties and taxes or a risk during an audit.

The right reflex is simple: never automatically reuse an old HS code without checking it.

DISCOVER OUR TRANSPORT SERVICES

Who pays import duties and taxes?

The payment of import duties and taxes mainly depends on the Incoterm, the commercial contract and the role of the importer.

In many cases, the buyer or importer pays the import duties and taxes.

But some Incoterms change this distribution.

Under DAP, the seller transports the goods to destination, but the buyer generally pays import customs clearance, duties and taxes.

Under DDP, the seller handles import customs clearance, duties and taxes.

You should not assume that the party organising transport necessarily pays customs duties.

A seller may organise transport to your warehouse while leaving duties and taxes at your charge.

Who is responsible in case of customs blockage?

In case of customs blockage, responsibility depends on the cause of the problem.

A blockage may come from a missing document, an incorrect invoice, an inconsistent HS code, an incorrectly declared origin, a vague product description, a product restriction, a customs inspection or an issue with the payment of duties and taxes.

The cause of the blockage must therefore be identified.

If the supplier provided an incorrect description, the problem may come from the supplier.

If the importer validated the wrong HS code, its responsibility may be involved.

If the documents were sent too late, the issue often comes from coordination between the parties.

If the customs representative declares the goods based on incorrect data, responsibility may depend on the mandate and the type of representation.

This is why roles must be clarified before shipment, not when the goods are already blocked.

The most common mistakes

1. Thinking the freight forwarder is responsible for everything

The freight forwarder coordinates the shipment, but it does not replace the company for product information, HS codes, customs strategy or contractual choices.

2. Choosing an Incoterm without understanding the consequences

A poorly chosen Incoterm can create unexpected costs or misunderstood responsibilities. It must be chosen before shipment, not when a problem occurs.

3. Reusing supplier documents without checking them

A supplier may use a vague description, a local HS code or an incomplete invoice. The importer must check critical data.

4. Not clarifying the type of customs representation

Direct and indirect representation do not have the same implications. The mandate being used must be clear before the declaration is filed.

5. Waiting for the blockage before looking for the responsible party

When goods are already blocked, every hour matters. Roles must be anticipated before shipment.

How to clearly divide responsibilities

To avoid misunderstandings, roles must be formalised before departure, during transport and at arrival.

Before departure, check the Incoterm, named place, commercial invoice, packing list, HS code, origin, EORI number, product restrictions, required certificates, name of the declarant and type of customs representation.

During transport, monitor departure dates, transport documents, possible requests, missing information, routing changes, estimated lead times and transit points.

At arrival, confirm the filing of the customs declaration, payment of duties and taxes, possible inspections, release of the goods, final delivery and documents to archive.

Nexline’s analysis

In an international shipment, responsibility should never be assumed.

It must be defined.

Transport may be well organised, but a flow can still be blocked if the roles are not clear.

The issue is therefore not only knowing who transports the goods.

It is also knowing who provides the data, who checks it, who declares, who pays and who responds to customs in case of a request.

At Nexline, the objective is to help companies secure this chain of responsibilities.

This involves a practical review of your flows, Incoterms, documents and customs constraints.

The goal is simple: to prevent a grey area between supplier, importer, carrier and declarant from becoming a delay, extra cost or blockage.

In brief