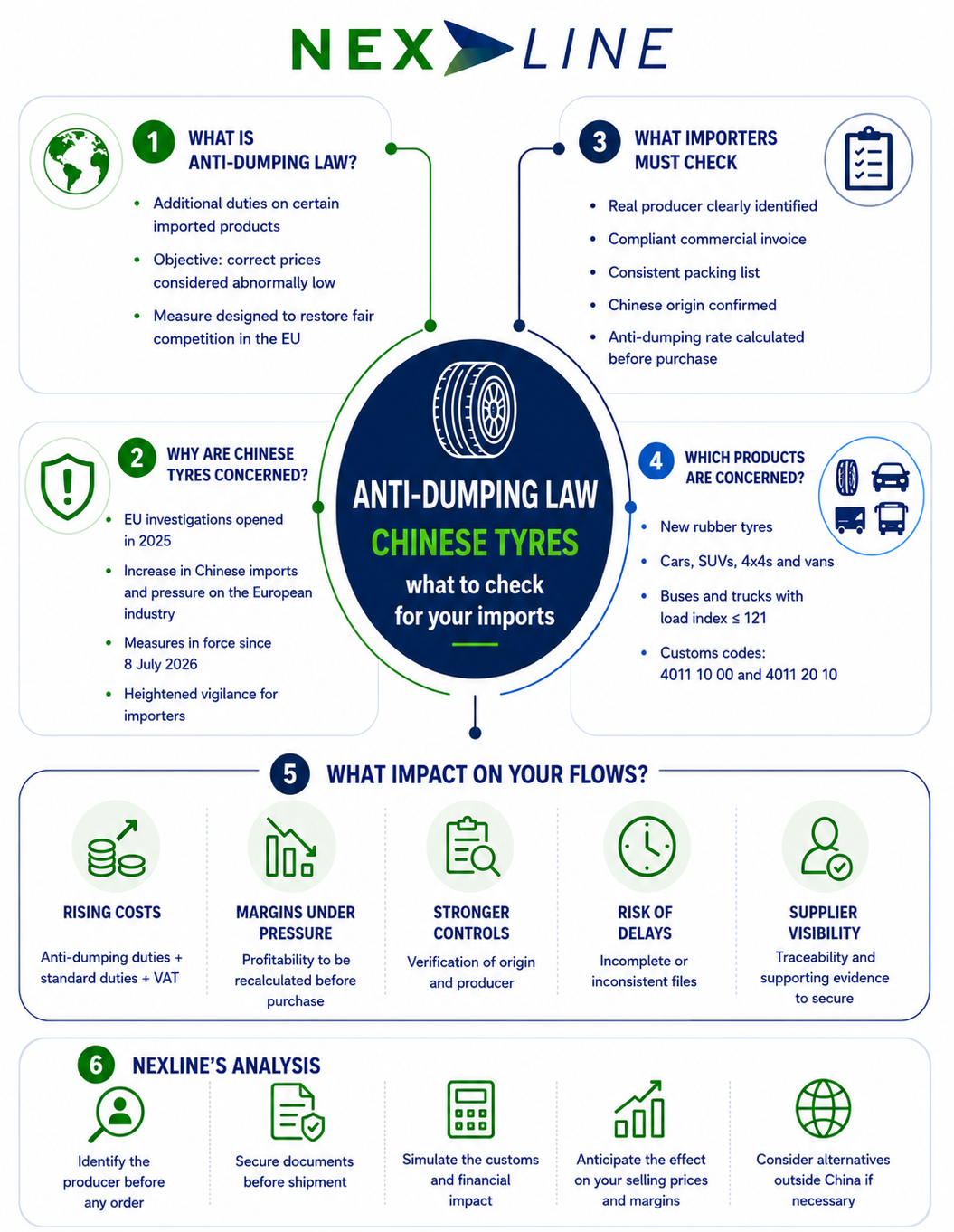

What is anti-dumping law?

Anti-dumping law allows the European Union to apply additional duties to certain imported products.

The objective is to correct a situation where goods are exported at prices considered abnormally low.

When these prices cause injury to European industry, the EU can impose anti-dumping duties.

In other words, this is not a general tax on all Chinese products.

It is a targeted measure. It applies to specific products, specific origins and, in some cases, specific producers.

To better understand this regulation, we will use a concrete and current example: the anti-dumping measures targeting certain new tyres originating from China.

Why are Chinese tyres concerned?

The European Union opened an investigation in May 2025 into Chinese tyres for passenger cars and light commercial vehicles.

The investigation followed a complaint from the European tyre industry, which considered that these imports were being sold at unfairly low prices and were causing injury to European producers.

Reuters reported that the European market for passenger car and light commercial vehicle tyres was worth more than €18 billion in 2024.

Another anti-subsidy investigation was also launched in November 2025 into certain Chinese tyres. According to Reuters, the complaint mentioned a 51% increase in Chinese imports since 2021, with prices 30% to 65% lower than those of European producers.

The objective of the measure is therefore to restore fairer competitive conditions.

Which tyres are concerned?

Anti-dumping law targets new rubber tyres originating from China.

The products concerned include tyres for:

- passenger cars;

- SUVs;

- 4×4 vehicles;

- vans;

- buses;

- trucks, if the load index is less than or equal to 121.

The customs codes mentioned are:

- 4011 10 00;

- 4011 20 10.

The key point is the real origin of the tyre.

A tyre purchased from an intermediary outside China may still be concerned if it was manufactured in China.

By contrast, used tyres, retreaded tyres or products outside the scope of the measure must be analysed separately.

What are the anti-dumping rates?

The duties vary depending on the Chinese producer.

| Producer category | Anti-dumping duty |

|---|---|

| Hankook producers concerned in China | 4.3% |

| Cooperating Chinese producers | 24.4% |

| Non-cooperating or not clearly identified producers | 45.3% |

The rate can therefore vary significantly depending on the manufacturer.

For an importer, this is not a detail.

On a customs value of €100,000, this represents:

- €4,300 with a 4.3% rate;

- €24,400 with a 24.4% rate;

- €45,300 with a 45.3% rate.

The difference can completely change the margin of an operation.

Why is the Chinese producer so important?

This is the most sensitive point.

The anti-dumping rate does not depend only on the seller. It depends on the actual producer of the tyre.

If the importer buys through a trading company, distributor or intermediary, they must still be able to clearly identify the production plant.

Otherwise, the maximum rate may apply.

To reduce this risk, the documents must clearly indicate:

- the legal name of the producer;

- the producer’s address;

- the country of origin;

- the link between the producer and the imported tyres;

- consistency between the invoice, packing list and customs declaration.

A vague commercial name is not always enough.

Customs authorities must be able to understand who actually manufactured the tyres.

Which documents should be prepared before shipment?

Anti-dumping law should not be managed only when the goods arrive.

It must be anticipated before the purchase and before shipment.

To secure the file, the importer should check several documents:

- commercial invoice;

- packing list;

- transport document;

- declaration of origin;

- full name of the producer;

- manufacturer’s certificate, if necessary;

- customs code;

- proof of production, if requested.

The most important point is consistency.

The invoice, packing list, origin and producer information must all tell the same story.

If the invoice only mentions a seller, without identifying the actual manufacturer, the file may become fragile.

What is the impact on import costs?

Anti-dumping duties are added to other costs.

They do not replace standard customs duties.

The full landed cost must therefore be simulated before confirming the order.

Mini-diagnosis: are your imports exposed?

Your company should ask the right questions before placing an order.

Answer yes or no:

- Do you import tyres from China?

- Are the tyres new?

- Are the customs codes 4011 10 00 or 4011 20 10?

- Is the load index less than or equal to 121?

- Do you know the actual producer?

- Is the producer’s name shown on the invoice?

- Is the packing list consistent?

- Do you have proof of origin?

- Have you simulated the applicable anti-dumping rate?

- Have you considered an alternative if the cost increases?

If several answers are uncertain, the file should be reviewed before shipment.

Common mistakes to avoid

- 1. Looking only at the supplier

- 2. Discovering the rate during customs clearance

- 3. Accepting a vague invoice

- 4. Mixing several producers in the same batch

- 5. Not keeping supporting evidence

What should importers do now?

Companies concerned by these measures should act before the next shipment.

The right method is to start by identifying all Chinese tyre flows.

Then, check the actual producers.

Next, simulate the financial impact based on the applicable rate.

Finally, update purchasing documents, invoices and sales conditions.

For some importers, it may also be necessary to review:

- selling prices;

- margins;

- customer contracts;

- supply sources;

- import routes;

- customs clearance timelines.

In some cases, an alternative source outside China may be relevant.

But it must be assessed carefully: price, availability, quality, compliance, lead time and production capacity all matter.

SECURE YOUR IMPORTS

Nexline’s analysis

For a company, the risk is not limited to paying an additional duty.

The real risk is discovering too late that the actual cost of the operation is no longer the cost expected at the beginning.

That is why the file must be secured before shipment.

The producer must be identified.

The rate must be simulated.

The documents must be consistent.

The impact on the margin must be anticipated.

At Nexline, the objective is to help importers make the right decisions before the goods are exported.

This includes analysing flows, checking documentation and simulating the customs impact.

The goal is simple: to prevent a poorly anticipated anti-dumping duty from becoming a cost, delay or profitability issue.

In brief